When Your VC Leaves, You Are Fundraising Again

A founder texted me this morning. His partner had just posted on X about leaving the firm, and he wanted to know how to manage the risk. I remembered a post Hunter Walk wrote in 2019 about exactly this, and if you haven’t read it, it’s worth finding. He covers the VC mechanics clearly. But after talking to many founders who’ve gone through it, I kept running into the same gap: the advice from inside the VC system assumes you understand how a firm works from the inside, and most founders don’t. So this is the founder’s side of the story.

Why it’s happening more

For a long time, getting check-writing authority at a venture firm took close to a decade. The title carried real weight because the partnership had already formed a view of you before you ever wrote a term sheet. Then the incentives shifted. Some firms started handing out partner titles broadly, for marketing, for volume, to compete for talent. Once that happened, more disciplined firms followed, because their junior investors would leave for the title elsewhere. A generation of investors started writing checks before the partnership fully believed in them. Some are exceptional and build long careers. Some move to better-branded firms. Some start their own funds. And some leave by choice, to start companies, to join the AI wave, to go somewhere their judgment fits better. The reason for leaving says nothing about what happens to you. VC departures are structurally more common than they used to be, and if your partner had check-writing authority, you are directly affected.

Two perspectives on the same situation

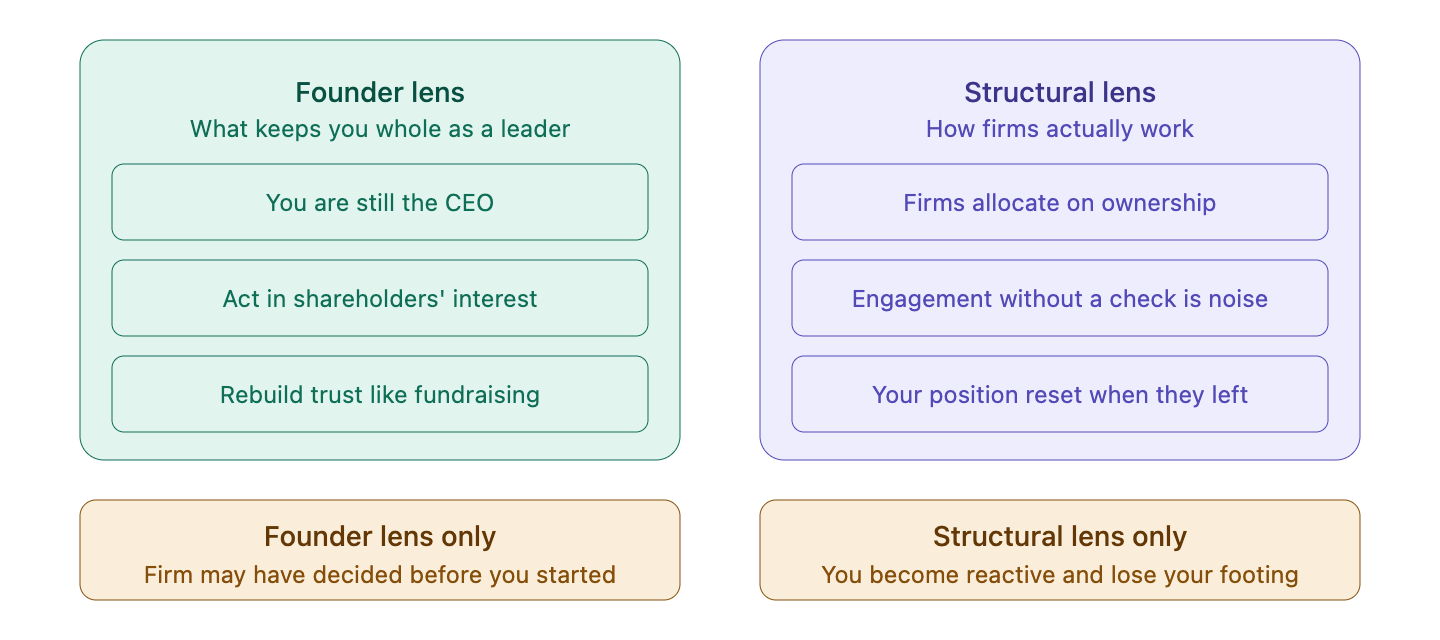

Before the tactical advice makes sense, it helps to know that two completely different lenses exist on this situation, and you need both of them.

The founder perspective says: you are still the CEO, and that doesn’t change because a partner left. Your responsibility is to act in the best interest of the company and its shareholders. You can disagree with investors about how to create value. That is part of the job. I’ve given this advice to founders before and heard experienced founders pass it to others: stay grounded, keep reinforcing your conviction, treat rebuilding internal support like fundraising. Consistency over months compounds. The people watching you hold your footing through a hard period will respect you for it later.

The structural perspective says: firms allocate attention and capital based on internal ownership, not warmth. When your partner left, your position inside the firm reset regardless of how the emails read. A partner who believes in your company will find a way to put more money in. Without a concrete signal of commitment, all the good conversations in the world tell you nothing about what the firm will actually do.

Use only the founder lens and you risk spending months rebuilding belief with people who have already moved on internally. Use only the structural lens and you make decisions from a defensive, cynical posture that costs you the credibility you need to re-earn support. You need both.

What changed when your partner walked out

When your VC leaves, your company gets re-evaluated inside the firm. Not in a meeting. Not in a memo. Just in where attention flows, who speaks up for your company in partner discussions, who uses their political capital on your behalf. The partner who wrote your check carried context that isn’t in any document: why you made the calls you made early, the reasoning behind bets that weren’t obvious yet, what made the thesis work before it was visible to others. That institutional memory left with them. From the outside, nothing looks different. Emails stay warm. Conversations still happen. But engagement without ownership is just politeness, and in a firm, ownership is the only thing that moves resources.

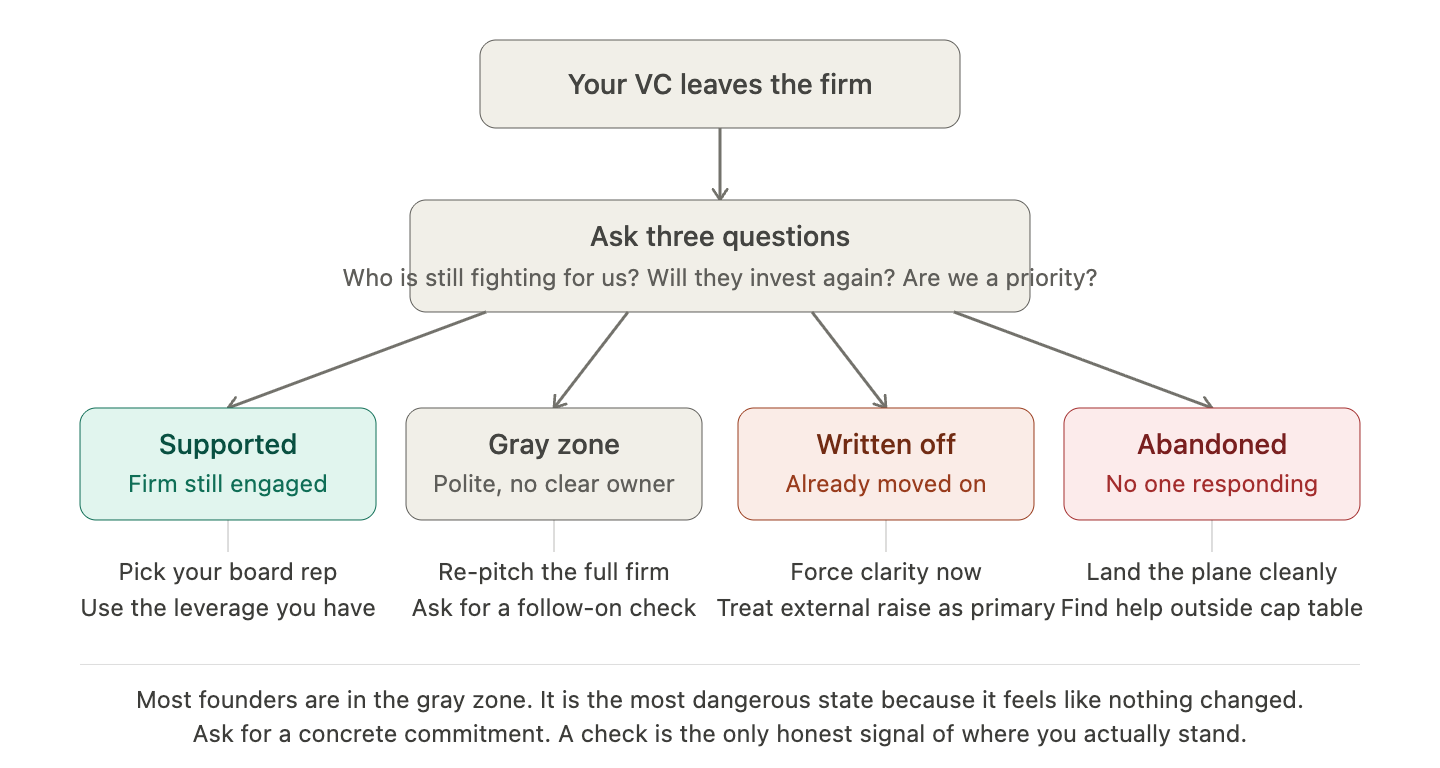

Diagnose before you do anything

Before you try to rebuild anything, you need to know where you actually stand. Ask directly: who owns us internally now? Under what conditions would the firm invest again? Are we still a priority for the partnership? These are uncomfortable questions, and most founders avoid them for that reason. Without answers, you’re operating on optimistic assumptions. Ask.

The gray zone: re-pitching is right, but it’s not enough

Most founders land in the gray zone. People are polite and the surface looks normal, which is exactly why it’s the hardest state to respond to correctly. The right instinct is also the one that gets executed incompletely. Yes, treat this like fundraising. Re-pitch the full partnership. Show what’s already working, not just what will work. Address the doubts you know exist but haven’t been voiced. Do this over months, not weeks. Rebuilding belief is slow.

Where founders get stuck is assuming that rebuilding the relationship is the goal. The actual goal is getting a concrete signal of commitment. Inside firms, the default behavior when things are uncertain is to stay supportive, avoid conflict, and defer hard decisions. You can have a run of strong conversations and interpret that as momentum. Often it isn’t. One pattern shows up repeatedly: a founder tries to gauge support before raising their next round, and the firm comes back with something that sounds reasonable. Go raise from the market, and if the round comes together, we’ll take our pro-rata. That’s not backing. That means the firm won’t take independent risk. They’re waiting for an external lead to validate the decision for them. If you’re in that position and you do need to raise, don’t wait for internal clarity before starting external conversations. Internal repair takes months. Starting external conversations early isn’t disloyalty. It’s an accurate read of the timeline.

When the system actually disappears

There’s a state that almost never gets addressed. You’re not just written off. No one picked up ownership after your partner left. Board members stop responding. Decisions that require governance stall because no one wants to be accountable, and no one wants to be seen as the person who let the company down. Sometimes the company has real options in this state: a potential acquirer, IP that could be sold, a strategic fit somewhere. And the people with fiduciary responsibility are nowhere to be found.

The board dynamics in this state can get structurally bad in ways that are often preventable earlier. If you remove a co-founder from operations, think carefully about whether they keep their board seat. A removed co-founder who is unhappy, with board rights and no operational role, can do real damage at exactly the moment when you need governance to function. And sometimes a board member knows what vote is needed but abstains anyway, because they don’t want their name attached to a hard decision. They’re protecting their own reputation, not the company. This is what I’ve called the Schrödinger’s VC: someone who preaches partnership before the deal and goes quiet when adversity arrives. The way to screen for it before you take someone’s money is to ask how they behaved when a portfolio company was struggling. Ask for a specific example, then go verify it directly with that founder. Character in adversity is the only reference check that matters. I talked through how to do this pre-investment on 20VC.

Find help outside the cap table

In the abandoned state, the instinct is to focus entirely on the investors who are supposed to be there. That’s the wrong frame. The most useful help often sits completely outside your existing cap table. Founders who have been through shutdowns, acquihires, or partial sales know the actual mechanics: which corp dev teams to talk to, how to position an asset sale, what an acquihire process looks like in practice. Those conversations cost nothing and are frequently more actionable than anything a checked-out board will give you. Reach out to former founders. Ask for specific introductions. Don’t wait for your investors to lead that effort. If a sale or acquihire becomes the real path, the mechanics of getting there are more specific than most founders expect. I wrote a detailed guide to early-stage M&A here, including how to build relationships with acquirers before you need them, what buyers actually value at the early stage, and why you need at least 9-12 months of runway before starting the process.

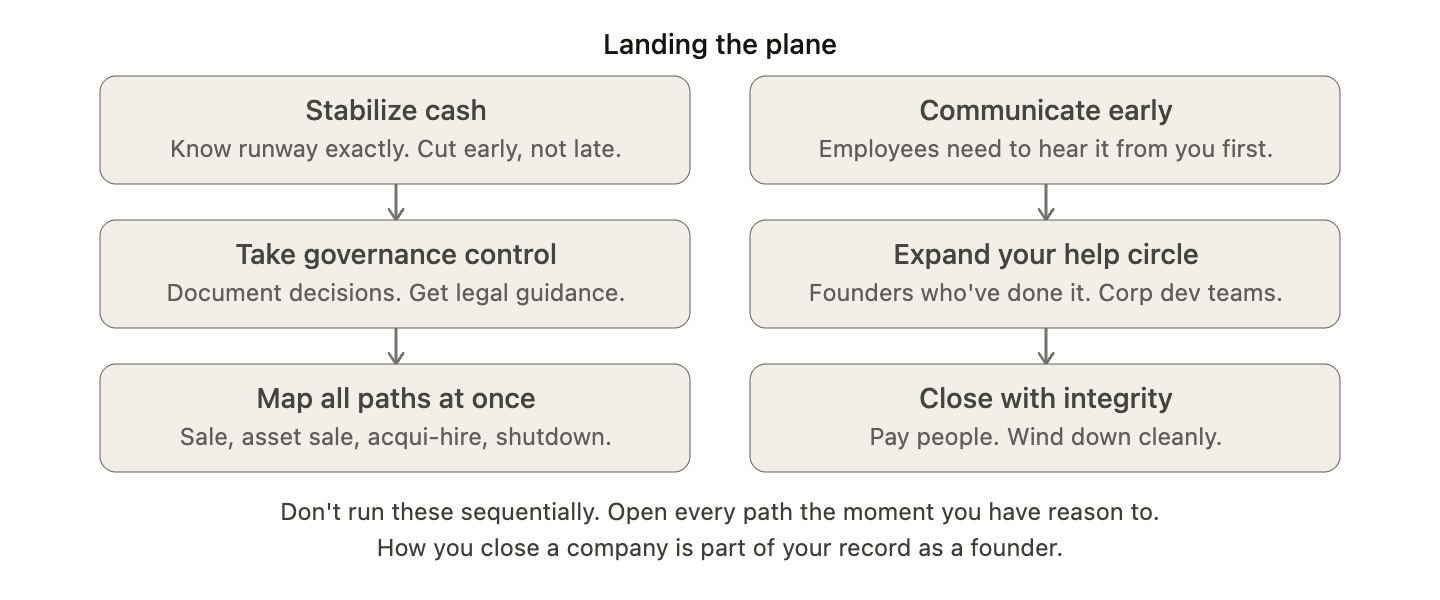

Landing the plane

Most outcomes are not venture-scale wins. Some are acqui-hires. Some are partial asset sales. Some are quiet shutdowns done carefully. How you move through any of these, whether people got paid, whether employees were told the truth early enough to make real decisions, whether you pursued every real option before closing, is part of your record as a founder. Companies deserve dignity at the end, not just at the peak.

When your VC leaves, the system reallocates its attention. Your responsibility doesn't. How you lead from that moment, how you diagnose clearly, how you communicate with your team, how you treat the people around you when things get hard, is exactly who you are as a founder. That doesn't change with a personnel announcement.

about Motive Force: Pre-seed & seed firm for founders who build before anyone asks. Backing Beautiful Software that amplifies human agency.

More essays: Your Sleep Debt is Diluting Your Equity, Founder Mental Software, Normalizing the Founder Journey, 7 Key Questions - learnings from my founder story